Airports Commission consultation launched – acknowledging it lacks the necessary information on carbon constraints

The Airports Commission has published its consultation about the 3 short -listed runway schemes (Heathrow north-west runway, Heathrow “Hub” and Gatwick). The Commission, rather than themselves assessing whether a runway could, or should, be built – adding to UK carbon emissions, leaves that part of policy to others. The CCC (The Committee on Climate Change) has advised that UK aviation emissions should not rise to over 37.5MtCO2 per year, from around 33MtCO2 now. The Commission has had trouble trying to incorporate a new runway at one airport, as well as growth at other UK airports, within the 37.5MtCO2 cap. All sorts of assumptions have to be made. At heart, the Commission has conceded that: “The Commission intends to carry out further work to complete a fuller economic assessment of the case where UK aviation emissions are constrained to the CCC planning assumption of 37.5MtCO2e for its final report in summer 2015.” ie. They do not have the necessary information on whether a runway could be viable, with the necessary price of carbon in future.

.

Tweet

Consultation document

The Commission says: (Page 25 of the consultation document)

“2.41 It has not been possible to assess the transport economic efficiency, delays or wider economic impacts under a carbon-capped forecast. This is because carbon prices are much higher in each scheme option than the ‘do minimum’ baseline, meaning the carbon policy component of the appraisal dominates the capacity appraisal. This is particularly problematic as appropriate carbon policies have not been investigated in detail. ”

[ In other words factoring in carbon costs would mean none of the schemes would look economically beneficial. Therefore The Commission has ignored them. ]

The whole of Para 2.41 states:

.

Airports Commission Consultation

Airports Commission on Gatwick (138 pages)

Gatwick Airport second runway: business case and sustainability assessment

Airports Commission on Heathrow Hub – extended northern runway – ENR (144 pages):

Heathrow Airport extended northern runway: business case and sustainability assessment

Airports Commission on Heathrow Airport’s own runway scheme (144 pages):

Heathrow Airport north west runway: business case and sustainability assessment

The detailed technical documents supporting the runway schemes

Technical documents (over 50)

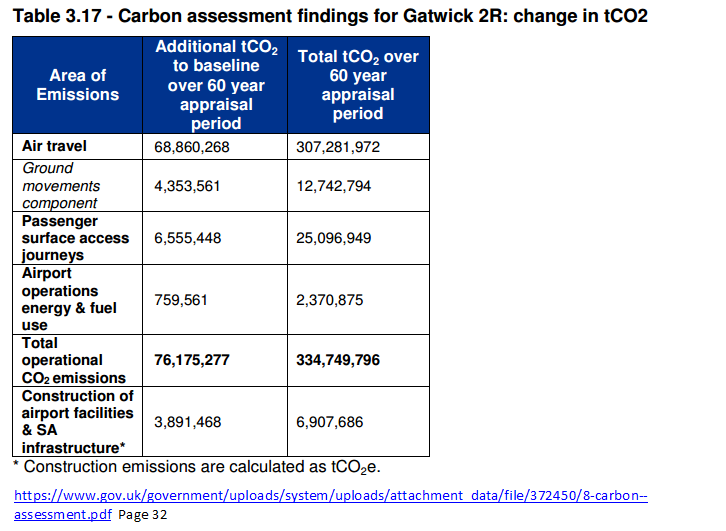

Consultation documents relating to carbon emissions

https://www.gov.uk/government/publications/additional-airport-capacity-carbon-analysis

1. Carbon Baseline (69 pages)

2. Carbon Assessment (153 pages)

It identifies the potential impact of the three proposed schemes in terms of carbon (dioxide) emissions. In establishing the baseline for a 60 year appraisal, the do minimum has a base date of 2025 for Gatwick 2R and 2026 for Heathrow NWR [north west runway option] and ENR [Heathrow Hub, extended northern runway] in line with assumed opening dates of ‘do something’ development, and corresponding end dates at 2085 / 2086. Comparisons for the years 2030, 2040 and 2050 are considered. The report assesses CO2 emissions in terms of:

– aircraft

– passenger surface access

– airport operations (energy and fuel use)

– construction activity

Below are sections referring to carbon emissions from the Airports Commission’s consultation document:

Future demand forecasts across a range of scenarios predict significant growth

in demand for aviation to 2050, placing additional pressure on already stressed

airport infrastructure in London and the South East. This includes forecasts in which

carbon emissions from aviation in 2050 are constrained to the 2005 level, in line

with the Climate Change Committee’s planning assumption for achieving the UK’s

2050 emissions target.

1.9

Without the provision of new infrastructure the London airport system is likely to

be under very substantial pressure in 2030, and demand will significantly exceed

total available capacity by 2050. The Commission looked at accommodating this

future demand through a variety of means, including measures to redistribute

traffic, or through using surface transport improvements to replace the need for

air movements. None of these options was found to be effective in reducing the

capacity shortfall, and some of the measures were found to reduce long-haul

connectivity and be carbon inefficient. For these reasons, the Commission

concluded that there is a case for at least one net additional runway in

London and the South East by 2030.

2.32

In line with the approach taken in the Interim Report, the Commission has also

prepared two sets of forecasts for each scenario based on different approaches to

handling carbon emissions from aviation: ‘carbon-capped’ and ‘carbon-traded’.

Both sets of forecasts assume that the total number of emissions are set with

reference to stabilisation targets aiming for a global temperature increase of equal

or close to two degrees Celsius, and aiming to ensure that a four degree Celsius

global temperature increase is reached only with very low probability (less than 1%).

The two forecasts are characterised by the following key differences:

• The Commission’s ‘carbon-capped’ forecasts model the levels of aviation demand expected in a world where carbon dioxide emissions from flights departing UK airports are limited to 37.5MtCO2e – the level recommended by the Committee on Climate Change (CCC) as a planning assumption to achieve carbon reductions across the whole UK economy of 80% over 1990 levels by 2050.(5) The ‘carbon-capped’ forecasts therefore increase the costs of carbon to ensure demand for aviation in the UK is reduced to stay within this planning assumption, and as such assume no trading of aviation emissions either within the UK economy or internationally (for example, under an EU Emissions Trading Scheme or any subsequent international global agreement).

• By contrast the Commission’s ‘carbon-traded’ forecasts model the levels of aviation demand in a future where carbon emissions from flights departing UK airports are traded at the European level until 2030 and thereafter traded as part of a liberal global carbon market. In contrast to the ‘carbon-capped’ forecasts these do not constrain emissions to a pre-determined level; rather, they reflect the demand response to DECC’s carbon values for appraisal.

Note (5) This assumes international aviation emissions are assigned to the UK economy on the basis of departing flights or bunker fuel sales in the UK, which is a relatively good proxy.

2.33 As with the Commission’s scenarios, the objective is not to identify a single ‘correct’ forecast, but rather to understand the varying effects on aviation demand of constraining and pricing carbon emissions. In effect the two worlds set out above represent a range of possible ways in which aviation in the UK may contribute to achieving stabilisation of the global climate.

2.34

2.34 At one end of the range the capped approach sees that happen within the UK economy. This takes a static view of what the relative effort between sectors should be, assuming no flexibility to promote economic efficiency or reflect society’s changing views of the value of aviation relative to other sectors. It is set with reference to the 37.5MtCO2e planning assumption the CCC recommends as a proxy until such time as a long-term global climate agreement is reached. This planning assumption has been developed with a view of what the relative effort of sectors should be based on what is known now – and thus reflects the CCC’s concern that should aviation emissions grow to 37.5MtCO2e, the implied 85% reduction in the CO2e emissions of other sectors may be at the limit of what is feasible. As the CCC notes it is a limit that should be kept under review, to allow for policy changes and new information about technology and abatement in different sectors.

2.35

The other end of the range assumes action to tackle emissions seeks the most globally economic efficient approach, without reference to national boundaries or other concerns that characterise current international negotiations.

2.36

The future reality is most likely to lie somewhere between these two worlds. For example, already today we can see a shift towards the international trading of aviation emissions through their inclusion in the EU emissions trading system, but also the international reactions to that and delays to its full implementation.

2.41

“It has not been possible to assess the transport economic efficiency, delays or wider economic impacts under a carbon-capped forecast. This is because carbon prices are much higher in each scheme option than the ‘do minimum’ baseline (8), meaning the carbon policy component of the appraisal dominates the capacity appraisal. This is particularly problematic as appropriate carbon policies have not been investigated in detail. For example, carbon emissions have been forecast assuming a rate of technological development and fleet turnover commensurate with past trends, whereas in reality it might be expected that the higher carbon prices associated with greater capacity could incentivise technological developments and uptake which enhance the carbon efficiency of aircraft. This risks implying greater dis-benefits attached to cutting carbon than may be realistic. The Commission intends to carry out further work to complete a fuller economic assessment of the case where UK aviation emissions are constrained to the CCC planning assumption of 37.5MtCO2e for its final report in summer 2015.”

Footnote (8): The Commission uses a ‘do minimum’ assessment to develop a baseline to compare the schemes against, which assumes no airport expansion at the three short-listed sites. In the case of both Heathrow schemes this do minimum case is based on Heathrow Airport Ltd’s most up to date Masterplan, and for the Gatwick scheme the respective Gatwick Airport Ltd Masterplan. These cover both what the airports are like now and agreed plans for how to develop the airport with no new runway.

3.16

entail increases in carbon emissions from aviation above 37.5 MtCO2e. The highest levels of emissions are associated with the low-cost is king and global growth scenarios, which would see UK aviation emissions in 2050 of 49-51 MtCO2e. If these emissions were not accounted for as part of a liberal global carbon market (as envisaged in this forecasting approach) and needed to be accommodated within any UK specific target this would see aviation emissions account for a larger share of the total and require commensurate reductions elsewhere in the economy, a situation in which the CCC advises it currently has ‘limited confidence. (Page 40).

3.67

While all of the carbon-capped scenarios keep carbon emissions from aviation at 37.5 MtCO2e in 2050, i.e. consistent with the Climate Change Committee’s advice, all the carbon-traded expansion scenarios entail increases in carbon emissions from aviation above that level. The highest levels of emissions are associated with the global growth and low-cost is king scenarios, which would see UK aviation emissions in 2050 of 50-51 MtCO2e. If these emissions were not accounted for as part of a liberal global carbon market (as envisaged in this forecasting approach) and needed to be accommodated within any UK specific target this would see aviation emissions account for a larger share of the total and require commensurate reductions elsewhere in the economy, a situation in which the CCC advises it currently has ‘limited confidence’.

For what it is worth, here are some more figures, but it is hard making sense of it all these documents …..