CCC confirm UK air passenger rise of 60% by 2050 only possible if carbon intensify of flying improves by one third

The Committee on Climate Change has reported to Parliament on progress on the UK’s carbon budgets. They say: “Under the current rate of progress future budgets will not all be met.” Carbon budgets do not currently include emissions from international aviation and shipping, but these are included in the 2050 carbon target. The government will review aviation’s inclusion in carbon budgets in 2016. In 2012 the UK’s international aviation emitted 32 MtCO2, and domestic aviation 1.6 MtCO2. The CCC and the Airports Commission say a new runway can fit within climate targets, but their own figures show aviation growth exceeding the target for decades. Growth in passengers of “around” 60% above 2005 levels could only fit within the carbon target if there is an improvement in the carbon intensity of aviation of around one-third by 2050. The Airports Commission’s own interim report says there can only be 36% growth in flights by 2050, to stay within targets. They say any more growth than that should not happen, “unless and until” there are the necessary technology improvements, cutting aviation emissions. But neither the government, nor the CCC, nor the Airports Commission can pin down what these will be, or when they will happen. UK aviation emissions remain the highest in Europe.

.

Tweet

Page 297 of CCC report http://www.theccc.org.uk/wp-content/uploads/2014/07/CCC-Progress-Report-2014_web_2.pdf

“We have previously suggested that returning aviation emissions to around 2005 levels in 2050 is an appropriate level of ambition. Both Airports Commission and CCC analysis suggest an additional runway by 2030 can be compatible with this approach, provided that aviation demand growth is limited to around 60% above 2005 levels and that there are significant improvements in carbon intensity of aviation (e.g. of around one-third by 2050).” Page 48 link CCC report

Policy strengthening required to meet future carbon budgets

15.7.2014 (Committee on Climate Change press release)

A new report (pdf) published today by the Committee on Climate Change (CCC) concludes that carbon budgets can be met at affordable cost, but that this will require the strengthening of key policies.

The CCC’s latest progress report to Parliament identifies that good progress has been made on development and implementation of some, but not all, policies. The first carbon budget has been met through successful low-carbon policies but also as a consequence of the impacts of the recession.

There has been strong progress in improving the fuel efficiency of new cars, as required by EU regulation, and in investing in wind generation under the Renewables Obligation. Foundations have been laid for the electric vehicle market and for demonstration of carbon capture and storage (CCS), although uptake of electric vehicles has been low and progress with CCS has been frustratingly slow. In other areas, progress has been limited, notably in energy efficiency improvement in the commercial and industrial sectors and in the uptake of heat pumps. Previous good progress in residential energy efficiency fell away with the new policy regime in 2013.

Under the current rate of progress future budgets will not all be met. Current policies may only reduce emissions by 21 to 23 per cent from 2013 to 2025, rather than the required 31 per cent reduction. To close this gap, the report recommends ways to increase uptake of energy efficiency improvement and investment in low-carbon technologies, supported by some behaviour change.

Achieving this will require further strengthening of policies, including the improvement to policy design and increased ambition, extended further in time. The CCC makes recommendations in the following specific areas:

Residential energy efficiency. Progress insulating homes plummeted with the introduction of new policies in 2013 (the Green Deal and Energy Company Obligation). For example, over 600,000 cavity walls were insulated in 2012 but only 170,000 in 2013. The Energy Company Obligation (ECO) is now being redesigned to include more low-cost measures and new financial incentives are being introduced for the Green Deal. This is welcome, but ambition remains low and should be increased.

Renewable heat. Increasing uptake of low-carbon heat is a priority. Despite the fact that the current scheme to incentivise this – the Renewable Heat Incentive (RHI) – is very generous, take-up of heat pumps has been very low (e.g. only around 1 per cent of spend to date in the non-domestic scheme). Rather than increase subsidy further, the Government should focus on tackling financial and non-financial barriers. This should include extending commitment and funding to the RHI beyond 2016, to reduce policy insecurity and encourage supply chain development, and allowing access to Green Deal finance for renewable heat installations.

Commercial sector. There is not much evidence of energy efficiency improvement in the commercial sector despite opportunities to do so. The policy landscape is complex and has mixed incentives. This situation should be simplified so that we lower administrative costs while, at the same time, improving delivery.

Power Sector. There has been progress on Electricity Market Reform, but there is a high degree of uncertainty about the support for low-carbon capacity beyond 2020. This undermines investment. It should be addressed by setting a carbon intensity target for 2030, together with funding to deliver this and strategies for commercialising offshore wind and CCS.

Electric Vehicles. While there have been some positive signals about the development of the electric vehicle market, the uptake of electric vehicles has been low. An ambitious EU target for new car emissions in 2030 would strengthen incentives for manufacturers to promote electric vehicles and develop innovative approaches to financing. This should be supported strongly by the Government. If put alongside further investment and development in charging infrastructure this could allow the current purchase subsidy to be phased out over time.

Action to cut emissions is increasingly important given progress that has been made towards ambitious new EU emissions targets, and the increase in the pace of international action. There is a clear economic benefit of acting now to cut emissions. This offers significant cost savings relative to delaying action, and will build a resilient energy system which is less reliant of fossil fuels.

Lord Deben, Chairman of the Committee on Climate Change, said: “Climate Change demands urgent action. We have started on the road and we are being joined by much of the rest of the world. However, despite our success, the UK is still not on track to meet our statutory commitment to cut emissions by 80 per cent. The longer we leave it, the costlier it becomes. This report shows the best and most cost-effective ways to ensure we meet our targets. There is no time to lose.”

http://www.theccc.org.uk/news-stories/policy-strengthening-required-to-meet-future-carbon-budgets/

.

Two new reports, by RSPB and by AEF/WWF on how a new runway cannot fit within UK carbon targets

WWF regional airports report re. climate – July 2014

Aviation Climate Change and Sharing the Load – RSPB July 2014

One page summary – Wing and a Prayer Event

…. more details …..

.

http://www.theccc.org.uk/publication/meeting-carbon-budgets-2014-progress-report-to-parliament/

Meeting Carbon Budgets – 2014 Progress Report to Parliament

This is our sixth statutory report to Parliament on progress towards meeting carbon budgets. In it we consider the latest data on emissions and their drivers. This year the report also includes a full assessment of how the first carbon budget (2008-2012) was met, drawing out policy lessons and setting out what is required for the future to stay on track for the legislated carbon budgets and the 2050 target. The report includes assessment at the level of the economy, the non-traded and traded sectors, the key emitting sectors and the devolved administrations.

Whilst the first carbon budget has been met, and progress made on development and implementation of some policies, the main conclusion is that strengthening of policies will be needed to meet future budgets.

Supporting data

- Chapter 2 (Excel)

- Chapter 3 (Excel)

- Chapter 4 (Excel)

- Chapter 5 (Excel)

- Chapter 6 (Excel)

- Chapter 7 (Excel)

- Chapter 8 (Excel)

.

Some extracts from the report, dealing with aviation:

UK greenhouse gas emissions including international aviation and shipping were 605 MtCO2e in 2013. Emissions in 2013 are now 25% below their 1990 level, and will need to fall a further 73% to meet the 2050 target. (Table 1). 1 Note 1: Carbon budgets do not currently include emissions from international aviation and shipping, but these are included in the 2050 target (see section 9).

—

Notes: *Emissions from international aviation and shipping are not currently included in carbon budgets, the government will review this in 2016. **Detailed emissions data for non-CO2 is not yet available for 2013; these figures assume the same % of total non-CO2

emissions for agriculture and waste as in 2012.

—

(i) Emissions trends

UK domestic transport CO2 emissions accounted for 25% (117 MtCO2 ) of all UK CO2

emissions in 2013. The majority of these are from surface transport (94%). Domestic aviation and shipping account for 3% with the remainder from other sources. Cars are the biggest contributor to surface transport emissions (58%), followed by heavy goods vehicles (22%) and vans (14%).

—

There are also 41 MtCO2 of emissions from international aviation (32 MtCO2 ) and shipping (9 MtCO2) – based on latest available data from 2012. These are not currently included in carbon budgets but are covered by the 2050 emissions target for at least an 80% reduction on 1990.

—

(iv) Aviation and shipping

In 2012 emissions from domestic aviation and shipping (included in carbon budgets) were 4.0 MtCO2, representing 3% of domestic transport emissions.

Emissions in aviation and shipping fell in the first carbon budget period, with reductions in

both domestic and international emissions (currently excluded from carbon budgets but in the

2050 target).

• Domestic aviation emissions fell 28%; international emissions fell 10%. This largely reflected

falling demand in the UK due to the economic crisis and improvements in fuel efficiency.

• Reductions in emissions from domestic and international shipping were both around 10%

over the first carbon budget.

In December 2013, the Airports Commission released its interim report which recommended

the need for an additional runway in the south east by 2030. It also suggested there could be

a case for a second additional runway by 2050.

We have previously suggested that returning aviation emissions to around 2005 levels in 2050 is an appropriate level of ambition. Both Airports Commission and CCC analysis suggest an additional runway by 2030 can be compatible with this approach, provided that aviation demand growth is limited to around 60% above 2005 levels and that there are significant improvements in carbon intensity of aviation (e.g. of around one-third by 2050). Executive Summary Page 48 link

[AirportWatch note: So the CCC says the UK can have another runway, as long as you do two other things, but it doesn’t spell out how or whether those two things can be technically accomplished, and also what the responsible parties have to do to achieve this. Ambiguity is thus inserted into the entire policy framework].

This approach should continue to be the basis for government policy unless and until

technology improvements allow higher passenger demand growth – and associated

infrastructure investment – to be demonstrated compatible with the 2050 target.

—–

Although not currently included in carbon budgets,

international aviation and shipping emissions are an important part of the 2050 target, and we

consider them in Chapter 5

—–

Total UK domestic transport CO2 emissions are provisionally estimated at 116.7 MtCO2

(25.1% of UK CO2 emissions) in 2013.

More detailed data are available for 2012, when total UK domestic transport CO2

emissions were 116.9 MtCO2 (24.7% of UK CO2 emissions), and total GHG emissions from domestic transport were 118 MtCO2 e (20.5% of total UK GHG emissions). Trends in non-CO2 emissions closely track those in CO2 (Figure 5.1).

Given the relatively low levels of non-CO2 emissions from domestic transport, the rest of this chapter will focus on CO2 emissions.

Total UK domestic transport CO2 emissions fell by 11.9% from 2007 to 2012, and a further 0.2%in 2013.

Surface transport CO2 emissions account for the vast majority of domestic transport emissions with domestic aviation and shipping accounting for 3%. The majority (96%) of surface transport emissions are from road transport and within this, the biggest contributors are cars (58%), vans (14%) and HGVs (22%)

—–

(ii) Emissions from aviation and shipping

Aviation

In 2012, at the end of the first carbon budget period, UK aviation emissions were 33.6 MtCO2

.

This represents a fall of 11% between 2007 and 2012 and a fall of 3% in the year ending 2012

(Figure 5.11). Both domestic and international emissions fell:

• Domestic aviation emissions fell by 4.4% in 2012 from 1.7 MtCO2 to 1.6 MtCO2

. Over the first carbon budget period they fell 28%.

• International aviation emissions (which are not included in carbon budgets) fell by 2.7% in

2012 from 32.8 MtCO2 to 32.0 MtCO2

. Over the first carbon budget period they fell 10%.

This reflects changes on both demand and supply sides:

• Demand for aviation fell substantially during the recession, and in 2012 was 8% lower than

in 2007.Chapter 5: Progress reducing transport emissions 261

• On the supply side, airlines reacted to falling demand by reducing the number of flights

(which fell by around 15% over the budget period) and by increasing the occupancy rate

of aircraft. Available data suggests fuel efficiency therefore improved (e.g. by an average of

1.6% per year over the first budget period4).

EU aviation emissions also fell over the first carbon budget period, by an average of 7% across both the EU-28 and EU-15. While UK emissions fell more, they remain the highest in Europe. This reflects the fact that UK passenger demand is the highest in Europe, as well as the UK’s role as an international long-haul hub.

4 Data from Sustainable Aviation Progress Report 2013. This covers emissions from all Sustainable Aviation partner airlines, including for their non-UK flights. It can therefore only

be considered indicative of changes in UK aviation fuel efficiency.

—–

5. Progress in reducing emissions from aviation and shipping

Recent developments in aviation and shipping policy at the international, EU and UK levels

reflect a continuation of approaches developed over the first carbon budget period:

• International – In October 2013 the International Civil Aviation Organisation (ICAO) agreed

a roadmap at their General Assembly for a market-based measure to control global aviation

emissions, to be decided at their 2016 General Assembly and to come into force in 2020.

The International Maritime Organisation (IMO) continues to support implementation of the

Energy Efficiency Design Index, agreed in 2011 and which entered into force in 2013.

• EU – In April 2014, following the ICAO’s agreement at their General Assembly, the EU

agreed to extend the “stop-the-clock” period for aviation in the EU ETS. This means that the

exemption of non-EU flights will continue until 2016 (i.e. only intra-EU flights are covered).

In June 2013 the European Commission proposed a new strategy for addressing shipping

emissions. The first stage proposes monitoring, reporting and verification of shipping

emissions from 2018 for ships using EU ports. This will help build a baseline for future stages,

with reduction targets and market mechanisms envisaged in the medium to long-term.

• UK – In December 2013 the UK Airports Commission released their Interim Report on future

UK airport capacity. This recommended the need for an additional runway in the south east

by 2030. This approach can be compatible with long-term objectives, if aviation demand growth is limited to around 60% above 2005 levels and provided that there are significant improvements in carbon intensity of flying (e.g. of around one-third by 2050) (Box 5.13).

In future both aviation and shipping emissions are projected to continue to rise absent further

measures but can be reduced through a combination of fuel efficiency improvements, use of

biofuels, and, in aviation, demand moderation to around 60% market growth by 2050. In our 2012 advice on inclusion of international aviation and shipping in carbon budgets, we agreed that appropriate planning assumptions for 2050 were for aviation emissions to be at around 2005 levels and for shipping emissions to be around one-third lower than 2010 levels.

More ambitious international policies, beyond those already agreed, will therefore be required to unlock the full range of abatement potential required.

To monitor annual progress, including towards these long-term objectives, we have developed – mirroring our approach for other sectors – a set of indicators for aviation and shipping. These summarise changes in aviation and shipping emissions, and the key drivers of these changes including demand and efficiency (Tables 5.4 and 5.5). We would welcome feedback on these indicators and will be further developing the evidence base underpinning them over the next year.

—————————-

http://www.theccc.org.uk/wp-content/uploads/2014/07/CCC-Progress-Report-2014_web_2.pdf

Page 297

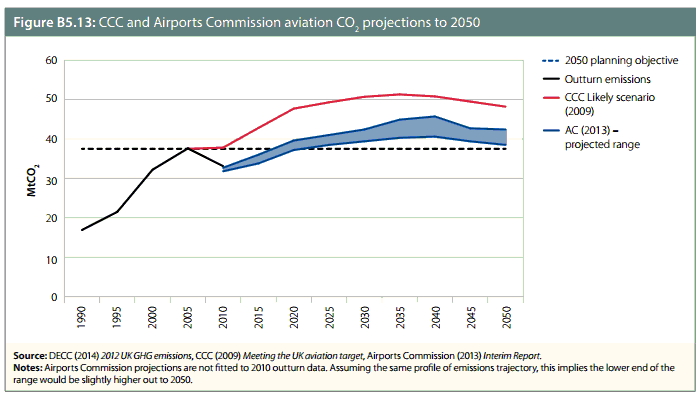

Box 5.13: The Airports Commission and future UK airport capacity

In September 2012 the Government established the Airports Commission to advise on future need for airport capacity in the UK. The Commission was asked to provide an interim report by the end of 2013 and final advice by summer 2015.

The Committee on Climate Change (CCC) wrote to the Commission in July 201333, highlighting that:

• Aviation emissions are included in the target to reduce economy-wide emissions by at least 80% in 2050 on 1990 levels, as set in the Climate Change Act.

• CCC analysis has illustrated how an 80% reduction could be achieved by returning aviation emissions to around 2005 levels in 2050, and reducing emissions in other sectors by 85% on 1990 levels.

• Returning aviation emissions to around 2005 levels in 2050 is possible through a combination of limiting demand growth to around 60% on 2005 levels, and significant reductions in carbon intensity

• Given the need to limit aviation demand growth in a carbon constrained world, this should be reflected in economic analysis of infrastructure investments. For example, these should assess whether investments still make sense where demand growth is limited to around 60%.

In December 2013 the Airports Commission released their interim report, which:

• Recommended the need for an additional runway in the south east by 2030 and suggested a number of options for siting this. Its analysis also suggested there could be a case for a second additional runway by 2050.

• Re-examined the level of aviation demand growth compatible with 2050 objectives. The analysis found an increase in demand of 67% would be compatible with returning aviation emissions to 2005 levels by 2050, very close to our previous conclusions.

• Concluded that the need for an additional runway by 2030 was valid across a range of future scenarios, including where demand growth was limited to around 60-70% by 2050.

The Airports Commission’s emission projections are broadly similar in profile to previous CCC analysis. Both show emissions which rise over time before flattening off. However, the Airports Commission’s projections are lower in bsolute terms and show aviation emissions closer to 2005 levels in 2050 (Figure B5.13). This largely reflects a lower starting point due to the recession, lower forecasts of future economic growth and changes in Government policy on

capacity expansion36.

[Note 36 The higher end of the Airports Commission’s scenario range reflects unconstrained airport capacity. The lower end of the range reflects current Government policy for no

new airport capacity. In contrast, CCC analysis was based on the then current policy of the 2003 Air Transport White Paper which assumed three additional runways by 2030 (at

Heathrow, Stansted and Edinburgh). ]

Both Airports Commission and CCC analysis suggest an additional runway by 2030 can be compatible with returning aviation emissions to around 2005 levels by 2050, provided that aviation demand growth is limited to around 60% above 2005 levels and that there are significant improvements in carbon intensity of aviation (e.g. of around one-third

by 2050).

This approach should continue to be the basis for government policy unless and until technology improvements allow higher passenger demand growth – and associated infrastructure investment – to be demonstrated compatible with the 2050 target.

The Airports Commission is now undertaking analysis to feed into their final report due in summer 2015, including investment and emissions appraisal of the runway options identified in their interim report. In their final report, the Commission should update their UK emission projections for each proposal to allow the long-term implications for 2050 to be accurately assessed.

We will continue to monitor trends in aviation emissions and key policy developments in the context of our annual progress reports to Parliament. We will also revisit aviation emissions and their inclusion in carbon budgets as part of our statutory advice on the fifth carbon budget, due by end-2015.

—-

.

Comment from an AirportWatch member on the report

The CCC annual progress report (http://www.theccc.org.uk/publication/meeting-carbon-budgets-2014-progress-report-to-parliament/ ) contains their assessment of the compatibility between the Airport Commission’s Interim Report and their own UK Carbon Budget.

The Airports Commission’s interim report, in December 2013 (in its technical appendix at https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/266670/airports-commission-interim-report-appendix-3.pdf

page 65 said:

“5.7 The new forecasts show that with carbon capped to the 2005 level of 37.5MtCO2 ,

passenger numbers in the unconstrained capacity case can increase by 65% and

ATMs by 33% above 2005 levels.62″

and footnote 62 says:

“62 The base 2005 levels are the full UK passenger and ATM totals of 229m and 160m respectively, as reported by the CAA and used by CCC. These totals include some passengers and ATMs at airports not included in the DfT modelling. If they were

excluded from the base, the growth rates would rise to 67% and 36% for passengers and ATMs”

ie. to keep UK aviation CO2 emissions to the level of 37.5MtCO2, there can be 67% more passengers, in 2050, than in 2005. And there can be 36% more ATMs than in 2005.

The CCC’s report is an artful piece of wording that leaves their own position substantially compromised:

– conclusion p.48 ‘Both Airports Commission and CCC analysis suggest an additional runway by 2030 can be compatible with this approach, provided that aviation demand growth is limited to around 60% above 2005 levels and that there are significant improvements in carbon intensity of aviation (e.g. of around one-third by 2050).’

– Box 5.13 pages 297-98 of the CCC report link has the detailed explanation. First it accepts that the CCC and AC forecasts ‘are broadly similar in profile’ when in fact they are significantly different in volume in relation to the critical ATM limit which it also doesn’t refer to.

The Airports Commission’s Technical Appendix 5.7 link said: “The new forecasts show that with carbon capped to the 2005 level of 37.5MtCO2, passenger numbers in the unconstrained capacity case can increase by 65% and ATMs by 33% above 2005 levels’ (footnote 62 increases those numbers to 67% and 36%); and now CCC says: ‘The [AC] analysis found an increase in demand of 67% would be compatible with returning aviation emissions to 2005 levels by 2050, very close to our previous conclusions.”

The Technical Appendix (pages 66 and 67) says:

“5.10 …..Figure 5.2 compares the destinations of the passengers modelled in 2050 in the two forecasts. Both assume that by 2050 long-haul flights carry 26% of passengers and are 12% of ATMs. The most obvious difference in the pattern of destinations is in the split between the domestic and short-haul passengers.”

“5.11 But the most significant difference between the CCC and Commission forecast is in the number of ATMs that can be accommodated within the carbon cap. While ATMs in the CCC forecasts grew by 55% from 2.2 to 3.4 million, in the new forecasts they grow by just 33% to 2.9 million. The difference is driven mainly by the modelling of, and underlying assumptions about, the loads on aircraft (passengers/ATM) and the distances passengers will be flying. Both assume that by 2050 long-haul flights carry 26% of passengers and are 12% of ATMs.”

The CCC no longer comment on the ATM compatibility issue. But it has changed from the CCC’s figure of 55% more ATMs in their 2009 guidance, to 36% more by the Airports Commission figures. This is due to use of larger planes, higher load factors, and a higher proportion of long haul flights,which emit more carbon per journey.

This is the most important manoeuvre by both bodies. What CCC said in 2009 link (page 26) was:

“The key implication from our analysis is that future airport policy should be designed to be in line with the assumption that total ATMs should not increase by more than about 55% between 2005 and 2050, i.e. from today’s level of 2.2 million to no more than around 3.4 million in 2050.”

The CCC use the figure of almost 2.2 million air transport movements (ATMs) in 2005. [CAA data ] If this increases by 55% by 2050, the total would be around 3.2 million ATMs.

If the 2.2 million ATMs grow by 36% by 2050, the total would be around 3.0 million.

Limiting the increase of ATMs now to just +36% of 2.2 million in 2005 (rather than 55%) in 2050 – means that 200,000 ATMs [or 400,000 ATMs taking the CCC number above] have to be taken off the capacity threshold, making it even more difficult to introduce new capacity/runways. But the CCC – as AC in the Interim Report – omit to point that out.

– This is followed by a second equally artful manoeuvre. CCC now says – referring again to Box 5.13, (on page 298) which states:

“Both [the CCC and the AC reports] show emissions which rise over time before flattening off. However, the Airports Commission’s projections are lower in absolute terms and show aviation emissions closer to 2005 levels in 2050 (Figure B5.13). This largely reflects a lower starting point due to the recession, lower forecasts of future economic growth and changes in Government policy on capacity expansion36.”

[footnote 36 The higher end of the Airports Commission’s scenario range reflects unconstrained airport capacity. The lower end of the range reflects current Government policy for no new airport capacity. In contrast, CCC analysis was based on the then current policy of the 2003 Air Transport White Paper which assumed three additional runways by 2030 (at Heathrow, Stansted and Edinburgh). ]‘

The text implies that AC are doing even better than CCC because their emissions projections are lower, whereas what the graph aboveshows is that:

(i) after 2010 (CCC) or 2020 (AC) both projections exceed the 37.5MtCO2 threshold

(ii) neither return it to 2005 levels by 2050*

– so the consequence of (i+ii) is a large cumulative exceedance through to 2050 – and in a situation where

(iii) the so called 37.5MtCO2 threshold – which is neither in or out of formal DfT policy – already takes up (with shipping) a whopping 25% of the 2050 UK carbon budget without any justification for that privileged grab.

But the CCC text again omits to point any of this out, and so portrays a significant breach of their own framework – as if it was some kind of success and compatibility.

[*As AC stated their intention of doing: ‘It therefore follows that emissions can, and do, exceed 37.5MtCO2 prior to 2050.’ Technical Appendix 5.4]

Section 5.4 (page 64 of link states:

“5.4 The targeted emissions level is met through supplementing the DECC price of traded carbon already included in the traded carbon scenario. This does not represent a new forecast of carbon prices, but is simply the value required, in the assumed absence of any other mechanism, to achieve the target of no more than 37.5MtCO2 from aircraft departing UK airports in 2050. The carbon price adjustment only aims at hitting the emissions level in 2050, as achieving the target earlier would require further transitions of the fleet and operational practices, fuels etc. beyond those included in the baseline. It therefore follows that emissions can, and do, exceed 37.5MtCO2 prior to 2050. Analysis by the CCC and the DfT has demonstrated that this target could be achieved by mechanisms other than the carbon price.61″

– Yet the overall thrust of this progress report is that the CCC UK carbon budget is now threatened by exceedance: “This is confirmed by the analysis in the report, which projects emissions in 2025 [for the UK as a whole] up to 60 MtCO2e/year above the level of the fourth budget. The cost of closing this gap is affordable … Achieving this will require further strengthening of policies – including those for residential and commercial energy efficiency, electrification of heat and transport, and power sector decarbonisation.” link page 11

Notice that transport is included in that list (and Page13-14 of the CCC report then provides a list of measures to increase surface transport decarbonisation) yet at the same time CCC is endorsing treating aviation as ‘not part of transport’ and then to be permitted to actually breach the UK carbon budget.

– Finally we have a last piece of equivocation which has the two organisations apparently in broad agreement. CCC report Page 48 Link: “Both Airports Commission and CCC analysis suggest an additional runway by 2030 can be compatible with returning aviation emissions to around 2005 levels by 2050, provided that aviation demand growth is limited to around 60% above 2005 levels and that there are significant improvements in carbon intensity of aviation (e.g. of around one-third by 2050).”

However, this is on the basis that:

(i) the AC/DfT are to be permitted to breach the CCC’s own UK carbon budget;

(ii) the apparent abandonment by CCC of their previous ATM threshold set at whatever level;

(iii) note the vagueness of the two ‘arounds’ what the AC is proposing; and

(iv) that there is no specification of how the ‘provided that’ [aviation demand growth is limited to …] is to accomplished.

So there is now a nice triangular game of ‘pass the parcel’: both the CCC and AC are stating that it is not their job and within their remit to set out the mechanisms by which demand should be limited to within a capacity/emissions threshold. And the DfT made sure that the Aviation Policy Framework (March 2013) remained ambiguous on the issue.

Government will now proceed to take a decision on capacity without having put in place, or even considered, any demand management measures.

Consequently the ’emissions constraint’ is effectively removed from the policy/decision framework, effectively in just the same way way as happened in the 2003 White Paper process – with disastrous results.

It is also neutered as a discussion point, meaning that the public debate for the next two years can remain focussed on the ‘how many runways?’ and ‘where?’ questions.

The question has to be asked: how do these documents so conveniently agree with each other to conveniently gloss over points which should be clarified, in order to let the issue of building a new runway continue without important issues being properly addressed.

The CCC’s press release http://www.theccc.org.uk/news-stories/policy-strengthening-required-to-meet-future-carbon-budgets/ contains no mention of the aviation issue. But its Chair does state: ‘.. the UK is still not on track to meet our statutory commitment to cut emissions by 80 per cent. The longer we leave it, the costlier it becomes. This report shows the best and most cost-effective ways to ensure we meet our targets. There is no time to lose.”

.

.

.

See also

Plans to fit a new south east runway within UK climate targets are based on a ‘wing and a prayer’ – rather than reality

Two new reports have been produced, which seriously challenge the Airports Commission’s claim that it is possible to build a new runway and still meet the UK Government’s climate change targets. The reports also argue that building a new runway in the south east would worsen the north/south divide, as growth at the regional airports would need to be constrained in order to ensure CO2 emissions from aviation fall to their 2005 levels by 2050. The RSPB report, “Aviation, climate change and sharing the load” and the WWF report, by the AEF “The implications of a new South East runway on regional airport expansion” demonstrate that if a new runway is built, commitments under the Climate Change Act cannot be met unless significant constraints are imposed on the level of activity at regional airports. Both reports illustrate that if aviation emissions were allowed to soar, that would impose costs on the rest of the economy rising to perhaps between £1 billion and £8.4 billion per year by 2050 as non-aviation sectors would need to make even deeper emissions cuts. The regulatory regime for aviation carbon emissions is still just aspirational. Contrary to the impression given by the government and the Airports Commission, the issue of climate in relation to airport expansion has not been resolved.

Click here to view full story…

The two reports:

WWF regional airports report re climate – July 2014

Aviation Climate Change and Sharing the Load – RSPB July 2014

One page summary – Wing and a Prayer. Event

.

.

.

.

.

.

.

.

.

.